Prime Minister Narendra Modi’s government faces growing pressure to reduce rising petrol and diesel prices by cutting taxes, but the reason for not doing so can be traced back to the early 2000s. Thanks to the previous governments’ generosity of keeping petrol and diesel prices low, the present and next governments face a bill of Rs 1.3 lakh crore to pay.

Retail fuel prices in many states, including the national capital Delhi, have recently topped Rs 100 per litre. Up to 60 percent of fuel prices are accounted for by various state and federal taxes. In the last financial year 2020-21, the central government collected Rs 3.72 lakh crore in excise duty on crude oil and petroleum products; while the state governments collected Rs 2.03 lakh crore in sales tax and VAT on petrol and diesel. In contrast, the government is required to redeem oil bonds worth over a lakh crore rupees.

Oil bonds: what are they?

The former prime minister Manmohan Singh’s UPA and Atal Bihari Vajpayee’s NDA both issued oil bonds as a replacement for cash subsidies to oil marketing companies (OMCs). Indian Oil Corp, HPCL, and BPCL were issued sovereign oil bonds, which were transferable, allowing these companies to raise cash immediately. The government would be responsible for paying interest and redeeming the notes at maturity. During that time, OMCs sold fuel at lower prices than international markets to keep it affordable. These companies received compensation from the government.

In the current fiscal year 2021-22, the government must repay Rs 20,000 crore in bonds and interest on outstanding oil bonds. For the next six years, the government has a total debt obligation of Rs 1.30 lakh crore. Dharmendra Pradhan (before the recent Cabinet reshuffle) attributed an increase in fuel prices to the UPA government’s issuing of oil bonds. A Congress-led UPA left lakhs of crores in dues, which the Modi government must pay in the coming years. On the international market, the price of crude oil has also increased, according to him. India imports 80 percent of its oil, which accounts for the rise in petrol and diesel prices.

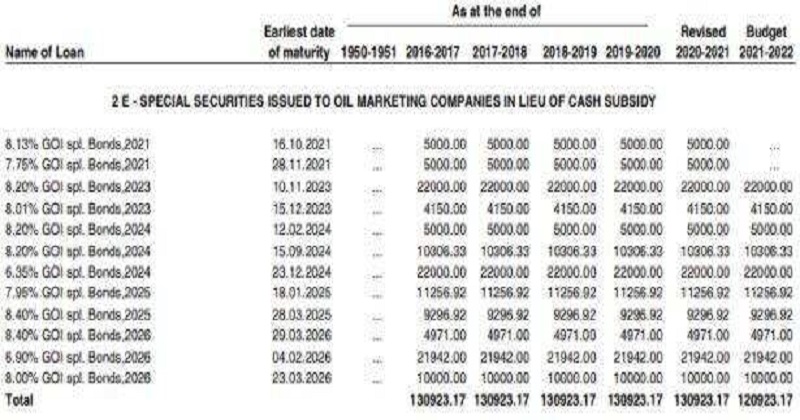

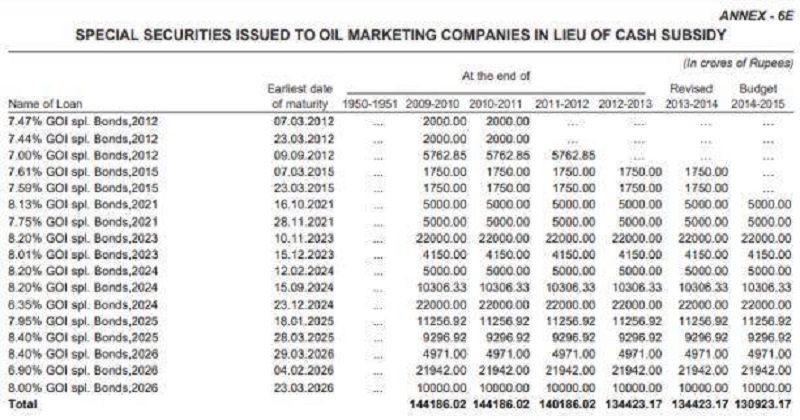

In a tweet, Amit Malviya, national president of the BJP’s IT cell, said the increase in petrol and diesel prices is a legacy of the UPA’s mismanagement. ‘We are paying for the oil bonds issued by UPA to oil companies to prevent them from increasing retail prices, bad economics, bad politics,’ (a part of the tweet read). In the receipt budget for 2021-22, according to annexure 6E titled ‘Special Securities Issued to Oil Marketing Companies in Lieu of Cash Subsidies’, pending liabilities related to oil bonds stood at Rs 1,30,923.17 crore. A total of Rs 1,30,923.17 crore was the value of pending oil bonds by the end of 2020-21. In 2014, Narendra Modi first came to power with the NDA government. There were two tranches of bonds maturing in 2015, each worth Rs 1750 crore (Rs 3500 crore).

Read more: Black Widow breaks pandemic records with $39.5 million at the box office

For the second consecutive year, Narendra Modi’s NDA government came to power. The budget documents state that oil bonds worth Rs 41,150 crore are due to mature between 2019 and 2024. During the last decade, Dharmendra Pradhan, Union Petroleum Minister, said that the government has paid around Rs 10,000 crore in interest. In the current fiscal year, the government is likely to pay a similar amount of interest on outstanding bonds. The total repayment and interest due on the oil bonds for the current fiscal year comes to approximately Rs 20,000 crore.

However, oil bonds were issued not only by the UPA government but also by the NDA government of Atal Bihari Vajpayee. In the 2002-03 budget speech, then Finance Minister Yashwant Sinha announced that oil bonds would be issued by the government. Oil Pool Accounts will not be maintained starting April 1, 2002, and the remaining balances will be liquidated through the issuance of petroleum bonds to the involved oil companies.

Post Your Comments